| Investment Spotlight / Contact Us / Proposal /; 繁體中文 } |

|

| Investment Spotlight / Contact Us / Proposal /; 繁體中文 } |

|

The internal audit system of Wah Lee Industrial Corp

1. Purpose of the internal audit:

To assist the board of directors and managers in promoting sound operations of the company and reasonably ensuring the objectives listed below are achieved. At the same time, to make timely recommendations for improvements to ensure sustainable operating effectiveness of the internal control system and to provide a basis for review and correction for the system.

1.1. Effectiveness and efficiency of operations,

1.2. Reliability of financial reporting, and

1.3. Compliance with applicable laws and regulations.

2. The Organization and Staffing of the Auditors Office:

The Auditors Office is under the board of directors. There are 1 chief auditor, several qualified senior auditors in the Auditors Office. The appointment or discharge of chief auditor is passed by the board of directors.

The personal information of the other auditors including their qualified conditions is reported to the FSC for recordation via the Internet-based information system by the end of January every year. The chief auditor reports audit performance to each supervisor on a regular basis and attends the board of directors meeting to report the situation of internal control in the Corporation.

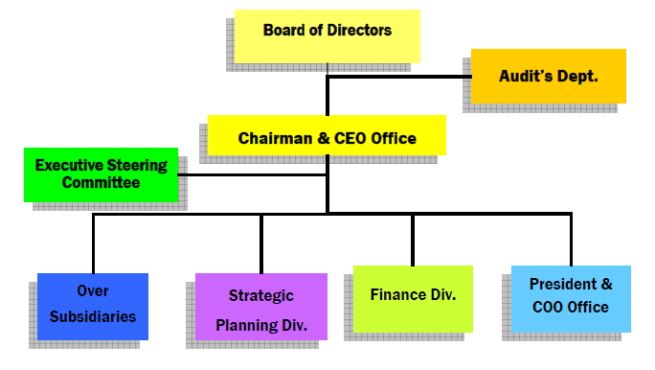

The organization Structure:

2. Internal Audit’s Functionality:

2.1. The scope of the Internal Audit: The scope of Internal Audit includes inspecting and reviewing the appropriateness and the effectiveness of internal controls system in each department of the company, and estimating the efficiency and effectiveness of operations. To be more specific, the scope of the internal audit includes:

2.1.1. Inspecting the reliability and completeness of the financial andoperating information.

2.1.2. Inspecting the current system to ensure the compliance of policies,plans, procedures, contracts, and laws.

2.1.3. Reviewing the securing of assets, and, if necessary, verifying theexistence of the assets.

2.1.4. Evaluating whether resources are being used economically and efficiently.

2.1.5. Reviewing the operations and special projects to ensure their results are consistent with the specified goals.

2.2. The Targets of the Internal Audit: The targets of the internal audit include all business units and subsidiaries this company is responsible for.

The staffs of the inspected unit should cooperate with the inspection closely.

2.3. The Method of the Internal Audit: In principal the inspecting staff should go to the unit for on site inspection and request the inspected unit to submit documents, accounts, certificates, etc. for documental

inspection.

2.4. The Internal Audit Work Process:

2.4.1. The internal audit includes the planning of inspections, the examination and estimation of information, the communication of the result, and the tracking after inspection.

2.4.2. In consideration of the risk, the annual plan of the internal audit should set major inspecting points for each individual case and keep journals of the audit.

2.4.3. After the inspection comes to an end, communicate with the director of the inspected unit regarding the results; when necessary,

acquire the improvement plan and the presumed date for completion. The inspecting staff should track the status of the improvement.

2.4.4. The inspection report and the tracking of abnormal issues should be reported to the Supervisors and the independent directors for review.

2.5. The Timing for the Internal Audit:

2.5.1. Regular Internal Audit: To ensure that the internal control of the company is effectively carried out, the Internal Audit Unit should set up the annual plan of inspection and determine the time of inspection for each inspecting item before the end of each year according to the characteristics of the trading cycle, the frequency of transactions of the company, and the complexity of operations.

2.5.2. Irregular Internal Audit:To fully understand the current situation of the inspected unit, the Internal Audit Unit may set up inspecting items regarding the importance, the risk, the frequency of transactions, and the complication of operations of each activities of the trading cycle.

2.5.3. Project Internal Audit:To ensure the effective implementation of the internal control of the company, the inspecting staff should launch inspections based on the time and the themes determined by the senior directors of the company or the director of the Internal Audit Unit.